We are Official Certified bubble.io & flutterflow App Development partner

.png)

Most founders love talking about building.

The product. The team. The traction. The raise. The growth metrics that are finally moving in the right direction.

What almost nobody wants to talk about is the end.

Not because they are not ambitious. Because "exit" sounds like giving up. Like admitting you are already planning to leave something you have not even finished building yet.

But that is not what an exit strategy is. Not even close.

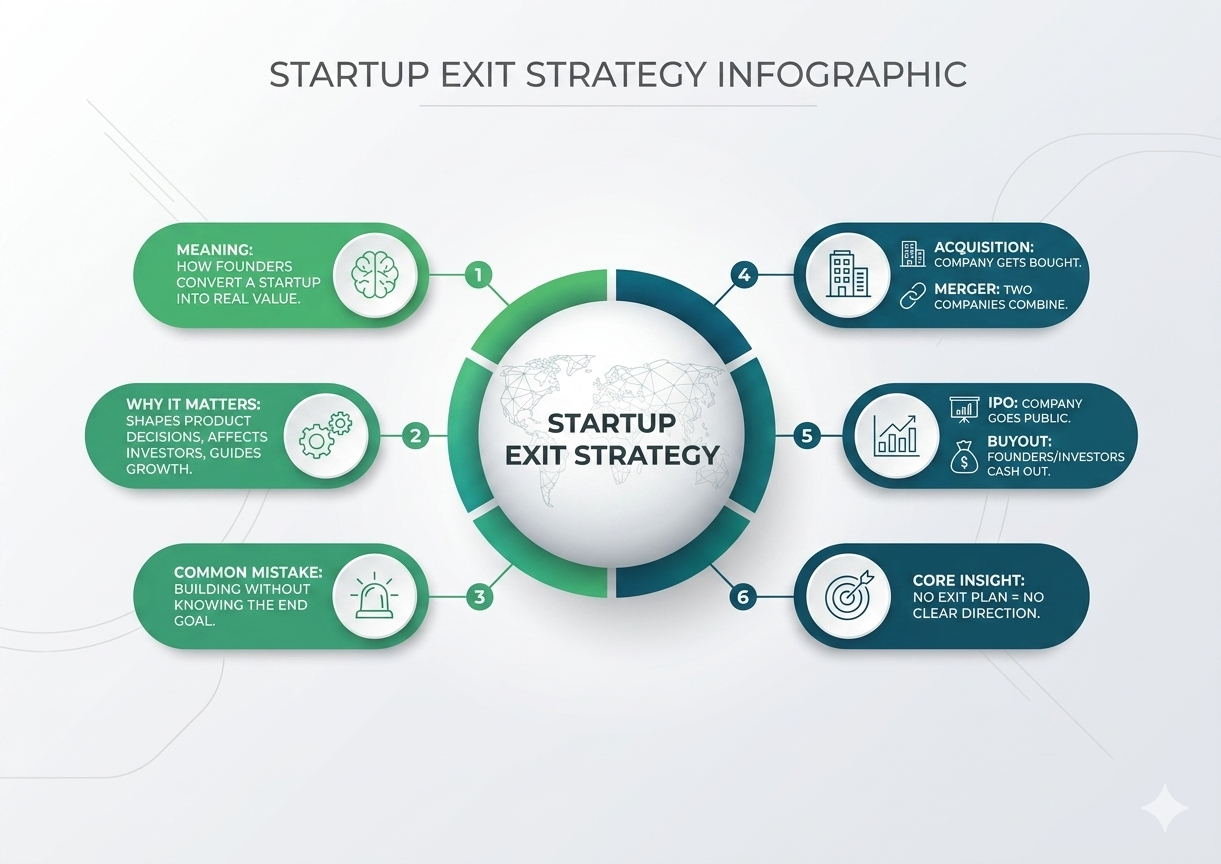

An exit strategy is not a plan to abandon your startup. It is a plan for how everything you are building eventually converts into real, tangible value for you, your team, and anyone who backed you along the way. It is the part of the roadmap that most founders leave blank and then scramble to fill in when an opportunity shows up unexpectedly or an investor starts asking questions you are not prepared to answer.

The founders who think about this early build differently. Better, usually. With more clarity about what actually matters and less time spent on things that do not move the company toward any meaningful outcome.

At its simplest, an exit strategy is a documented plan for how founders and investors will eventually convert their ownership into value.

That could look like several different things depending on the company, the market, and what the founders are trying to build toward.

It might mean selling the company outright to a larger player. It might mean going public through an IPO. It might mean a merger with a complementary business. It might mean a partial sale where founders take some money off the table while staying involved in the company.

None of these options are better or worse in the abstract. They are appropriate or inappropriate depending on the specific situation, the goals of the people involved, and the state of the company at the time.

What matters is that the question gets asked deliberately, early, and honestly, rather than getting deferred until someone else forces it onto the agenda.

To explore how exit strategies are structured across different business models, this resource explains the key approaches in detail: https://www.airswift.com/blog/business-exit-strategy

Here is the version of events that plays out more often than it should.

A founder builds a product, raises some money, gets traction, and at some point an investor asks: what does the exit look like? The founder gives a vague answer about potentially getting acquired someday or maybe going public eventually. The investor nods. But something shifts in the room.

That vagueness is expensive. Not because investors need a rigid plan. Because the exit question is really a proxy for a deeper one: do you understand what you are building toward and why?

Your exit strategy directly shapes decisions you are making right now. How you structure the business. Whether you raise outside funding and from whom. How fast you grow and whether that growth is the kind that attracts acquirers or the kind that just adds complexity. What features you build and which ones you skip.

At InceptMVP, the pattern is consistent across the startups we have worked with. Founders who think about exit early tend to make cleaner product decisions, structure their financials more carefully, and build things that hold value beyond the initial launch. Not because they are smarter. Because they have a direction, and direction makes every smaller decision easier.

This is how most startups exit. A larger company buys the startup, typically for the product, the user base, the technology, or some combination of all three.

Acquisitions happen across a wide range of sizes. Some are small acqui-hires where the team is the primary asset. Others are significant transactions based on revenue, user numbers, or strategic positioning.

What makes a startup acquirable is having something a larger company wants and cannot easily build themselves. A specific user base in a niche they are trying to enter. A technology that would take them two years to develop internally. A market position they would rather buy than compete with.

If acquisition is a likely exit for your company, the implication is that you should be building with a potential acquirer in mind. Not in a cynical way. In a practical one. What would make this company genuinely valuable to someone else in three to five years?

A merger happens when two companies combine because the combined entity is stronger than either one separately. This is less common for early-stage startups but becomes more relevant as companies mature and look for ways to accelerate growth or enter new markets without starting from scratch.

Mergers require significant alignment between both parties, not just on financials but on culture, leadership, and strategic direction. They tend to be slower and more complex than acquisitions.

Going public is the exit that gets the most attention and happens the least often.

An IPO requires strong, consistent revenue. Scalable operations that can withstand public market scrutiny. A growth story that holds up under quarterly reporting pressure. Legal, financial, and governance infrastructure that most early-stage companies are years away from having.

It is a legitimate goal for a specific kind of company. But treating it as the default exit plan without the substance to back it up is a mistake that wastes time and creates unrealistic expectations with investors.

This option gets overlooked in the typical exit conversation, but it is worth understanding.

A partial exit allows founders or early investors to sell a portion of their shares, either to new investors or to the company itself, while remaining involved in the business. It provides liquidity without requiring a full sale.

This can make sense when a founder has been building for several years and wants to reduce personal financial risk while continuing to grow the company. It requires the right investor relationships and a company that is generating enough value to make the transaction worthwhile.

The first question is the most personal one. Do you want to build a long-term company that you run for decades? Or something that reaches a specific scale and then becomes more valuable to someone else than to you?

Both are completely valid answers. The path is just different. And the product decisions, hiring decisions, and funding decisions that follow are different depending on which one is true.

If you have a co-founder, this conversation needs to happen between the two of you before it needs to happen with anyone else. Misalignment on exit vision between co-founders is one of the most damaging things that can happen to a startup, and it almost always surfaces at the worst possible time. Choosing the right direction also depends on who you build with, which is why understanding How to Select the Right Co-Founder becomes essential early on.

Different investors have different timelines and different definitions of success. Some want a return within five years. Others are comfortable with a longer horizon. Some push for acquisition. Others want to hold for an IPO.

If your exit vision does not match your investor's expectations, that tension will show up in board meetings, in strategic decisions, and in moments where you need unified support to do something important.

Ask the question directly before closing any investment. What does success look like to you at the end of this? What timeline are you working with? What exit outcomes are you hoping for?

The answers tell you whether the backing you are taking is genuinely aligned with where you are trying to go.

Companies do not get acquired because they exist. They get acquired because they have built something another company genuinely wants.

That means a strong and defensible user base. Proprietary technology or data that is difficult to replicate. A clear and well-understood market position. Clean financials that hold up under due diligence.

Every major product decision should pass a simple filter: does this make the company more valuable, or does it just make it more complex? Those are not the same thing. Complexity for its own sake is one of the fastest ways to reduce a company's appeal to potential acquirers.

The real shift happens in execution, and that process is covered in Complete Guide to Launching an App.

Messy finances are a deal killer. Not because acquirers cannot handle complicated books, but because the process of cleaning them up is expensive, slow, and creates doubt about what else might be disorganized.

Clean records, clear revenue recognition, documented expenses, and proper accounting from early on make due diligence faster and give buyers confidence. They also make it easier to present a credible story about the business to investors at any stage.

This is not just about exit preparation. Clean financials make the entire company easier to run. They surface problems earlier and give founders a more accurate picture of what is actually happening.

An exit strategy is a direction, not a script.

Markets shift. Competitors get acquired. New players enter. An acquirer you never considered shows up with an offer that changes the conversation. The conditions that made one exit path attractive in year two might look completely different by year four.

Smart founders revisit the exit strategy periodically. Not obsessively. But deliberately, at meaningful milestones, to ask whether the direction still makes sense given what has changed.

Waiting too long to think about exit is the most common one. By the time an opportunity shows up, the window to prepare is already closed.

Building without any clear outcome in mind leads to growth that looks impressive on a slide but does not translate into actual value. User numbers that do not convert. Revenue that does not scale. A product that is interesting but not defensible.

Misalignment with investors on exit expectations creates friction at exactly the moments when you need the most clarity and support.

Overvaluing too early, either by raising at an inflated valuation or by anchoring internally on an unrealistic number, makes future fundraising harder and can kill acquisition conversations before they start.

A deeper financial perspective on exit strategies and how they function in investment planning is explained here: https://www.investopedia.com/terms/e/exitstrategy.asp

The best founders are not the ones who are constantly thinking about the exit. They are the ones who understand it well enough to build toward it without being distracted by it.

An exit strategy is not an escape plan. It is a clarity tool. It helps you make better decisions now because you understand what you are trying to create and why it would matter to someone beyond yourself.

Build something valuable. Keep the structure clean. Align the people around you on where it is going. The exit takes care of itself when the foundation is right.

If you are in the early stages of building and want a product development partner who thinks about the full picture, not just the code, that is exactly what InceptMVP does. Work With Us

From the beginning, or as close to it as possible. Exit strategy influences how you build, what kind of investors you take, and the decisions you make at every major milestone. Waiting until an opportunity arrives means making important decisions without preparation.

Acquisition is by far the most common exit for early and growth-stage startups. A larger company purchases the startup for its product, technology, users, or market position. IPOs are significantly rarer and require a level of scale and infrastructure most startups take many years to reach.

If you are raising outside funding, yes. Investors need to understand how they will eventually see a return. Even if you are bootstrapped, having a clear direction for what you are building toward makes product and business decisions more focused and more consistent.

Significantly. If acquisition is the goal, you build with potential acquirers in mind, focusing on what makes the product uniquely valuable and defensible. If IPO is the direction, you build with scalability, clean financials, and repeatable growth as the priority. The exit shapes the architecture of the company long before the exit happens.

Ignoring it entirely until it becomes urgent. By the time an acquisition conversation starts or an investor asks for a clear exit path, the time to prepare has already passed. Founders who plan early have more options, better positioning, and significantly more leverage in any exit conversation.

.svg)

.svg)

.png)

.png)

.avif)